All Categories

Featured

Table of Contents

If George is diagnosed with a terminal ailment throughout the initial plan term, he possibly will not be eligible to renew the plan when it ends. Some policies offer ensured re-insurability (without evidence of insurability), but such functions come with a higher price. There are numerous types of term life insurance policy.

The majority of term life insurance coverage has a level costs, and it's the type we have actually been referring to in many of this write-up.

Term life insurance policy is eye-catching to youngsters with youngsters. Moms and dads can obtain significant insurance coverage for an affordable, and if the insured passes away while the plan holds, the household can rely upon the survivor benefit to replace lost revenue. These plans are also appropriate for individuals with expanding family members.

Why Life Insurance Is an Essential Choice?

Term life plans are optimal for individuals that want considerable insurance coverage at a reduced expense. People who possess entire life insurance policy pay much more in premiums for much less protection however have the protection of knowing they are protected for life.

The conversion motorcyclist need to allow you to convert to any type of permanent plan the insurance provider supplies without restrictions. The key functions of the biker are keeping the initial health ranking of the term plan upon conversion (also if you later on have wellness concerns or end up being uninsurable) and determining when and just how much of the coverage to convert.

Of course, total premiums will increase significantly because entire life insurance policy is extra pricey than term life insurance policy. Medical problems that develop throughout the term life period can not create costs to be enhanced.

What is Short Term Life Insurance? Detailed Insights?

Entire life insurance coverage comes with substantially greater month-to-month costs. It is suggested to give protection for as long as you live.

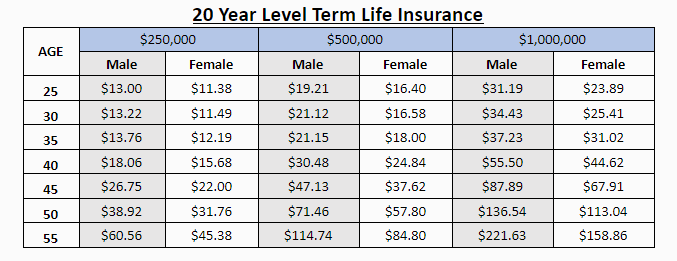

Insurance firms established an optimum age limitation for term life insurance policy policies. The costs likewise rises with age, so a person matured 60 or 70 will pay considerably even more than somebody years more youthful.

Term life is somewhat similar to auto insurance policy. It's statistically not likely that you'll need it, and the premiums are cash down the drain if you don't. If the worst occurs, your family will get the benefits.

How Does Guaranteed Level Term Life Insurance Protect You?

Essentially, there are two types of life insurance coverage plans - either term or permanent strategies or some mix of both. Life insurers supply numerous kinds of term strategies and typical life policies in addition to "interest delicate" products which have become more widespread because the 1980's.

Term insurance provides security for a given duration of time. This period might be as brief as one year or offer protection for a specific variety of years such as 5, 10, two decades or to a defined age such as 80 or in many cases up to the earliest age in the life insurance mortality.

What is Term Life Insurance For Seniors? A Guide for Families?

Presently term insurance policy prices are very competitive and amongst the most affordable historically experienced. It ought to be noted that it is an extensively held idea that term insurance coverage is the least expensive pure life insurance policy coverage available. One requires to assess the policy terms very carefully to make a decision which term life alternatives are ideal to fulfill your particular conditions.

With each brand-new term the costs is raised. The right to renew the policy without evidence of insurability is a crucial advantage to you. Otherwise, the risk you take is that your health and wellness might degrade and you may be not able to acquire a policy at the very same rates or also at all, leaving you and your recipients without protection.

The length of the conversion duration will differ depending on the type of term policy bought. The premium rate you pay on conversion is normally based on your "present obtained age", which is your age on the conversion day.

Under a level term policy the face amount of the plan continues to be the very same for the entire period. With decreasing term the face amount decreases over the period. The premium stays the exact same yearly. Usually such policies are marketed as home mortgage protection with the quantity of insurance lowering as the equilibrium of the home mortgage reduces.

Traditionally, insurance firms have actually not can transform premiums after the policy is offered. Given that such plans may continue for several years, insurance firms must utilize conservative mortality, interest and cost price estimates in the costs estimation. Flexible costs insurance policy, nevertheless, enables insurance firms to offer insurance coverage at lower "existing" costs based upon less traditional assumptions with the right to transform these costs in the future.

What is Level Premium Term Life Insurance? A Simple Breakdown

While term insurance coverage is developed to offer protection for a defined time period, irreversible insurance coverage is designed to supply coverage for your entire life time. To keep the premium rate level, the premium at the more youthful ages exceeds the actual expense of security. This added costs constructs a book (cash money value) which aids pay for the policy in later years as the cost of security surges above the costs.

Under some plans, premiums are called for to be spent for a set variety of years (Voluntary term life insurance). Under other policies, costs are paid throughout the insurance policy holder's life time. The insurer invests the excess costs bucks This sort of policy, which is often called cash money value life insurance policy, creates a cost savings component. Cash worths are important to a permanent life insurance plan.

In some cases, there is no relationship between the size of the cash value and the premiums paid. It is the cash money value of the plan that can be accessed while the policyholder is active. The Commissioners 1980 Criterion Ordinary Mortality (CSO) is the current table used in computing minimum nonforfeiture values and policy gets for common life insurance policy policies.

Why Short Term Life Insurance Matters

Lots of permanent plans will certainly contain arrangements, which define these tax obligation requirements. Traditional whole life policies are based upon long-lasting quotes of cost, rate of interest and mortality.

{kind=link}

Latest Posts

Does Medicare Cover Funeral Costs

Instant Whole Life Insurance

Life Insurance Quotes Instant