All Categories

Featured

Table of Contents

To offer a concrete instance of this, I just recently had a customer acquire instant-issue coverage at $126/month with a favored, non-tobacco score. Later on, he determined he wished to get commonly underwritten insurance coverage, which had the prospective to lower his premium to $112/month, thinking that underwriting would certainly preserve his recommended, non-tobacco rating.

Had he gone right for the traditionally underwritten protection, it would have finished up costing him dramatically extra. Naturally, there are drawbacks to instant-issue insurance coverage as well. Among one of the most evident drawbacks is the expense. While prices can range service providers and for different quantities at different score classes, with instant-issue protection, applicants can typically anticipate to pay a costs of a minimum of 1020% more than the most affordable commonly underwritten insurance coverage offered on the marketplace.

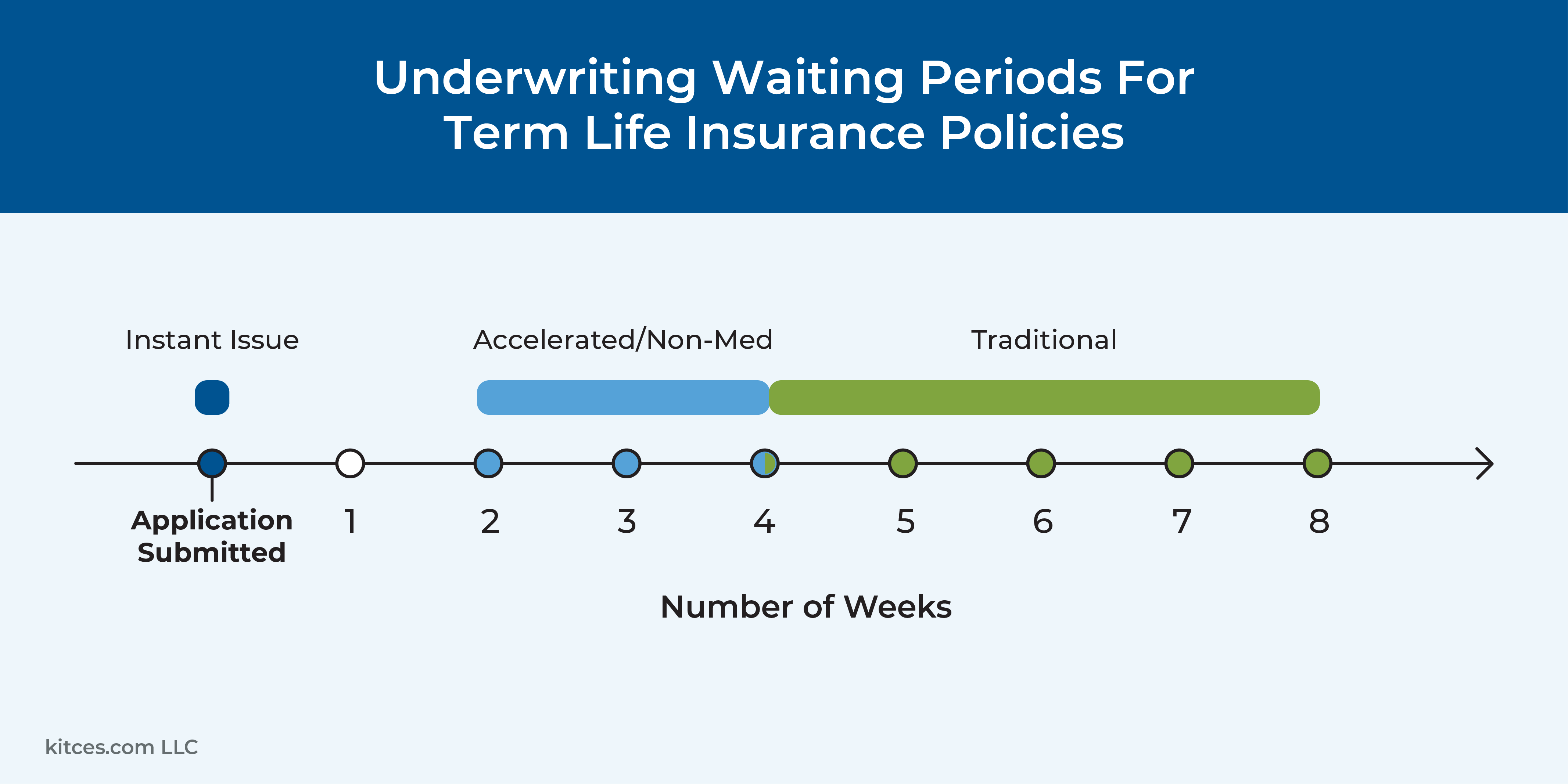

On the existing market, most instant-issue plans cap protection at $1 million to $2 million of death benefit. If they are going to go via the headache of traditional underwriting to obtain their wanted coverage in place, then it could make more feeling just to obtain all of that protection with conventional underwriting.

This is a viable method to obtain $5 million in protection, in addition to simply looking for $5 million of commonly underwritten insurance coverage with the intent to change the $2 countless instant coverage if the insurance coverage is provided at an extra desirable price. Insurance coverage limitations are absolutely a variable that requires to be thought about when choosing what type of underwriting to go via.

Free Instant Whole Life Insurance Quotes

Life insurance policy plans will normally have a 2-year incontestability duration. In the absence of scams, the incontestability stipulation avoids a life insurance policy business from contesting a policy once it has remained in area for 2 years. An instance might assist highlight why a medical examination can be valuable: John obtains term life insurance policy and precisely states his current weight at 150 pounds.

In the instance above, if John underwent traditional underwriting, it's going to be extremely clear that there was no scams or misrepresentation below. The insurance provider conducted their own physical of John and validated that he really weighed 150 extra pounds at the time of application. By comparison, expect John instead made an application for instant-issue insurance coverage.

Free Instant Whole Life Insurance Quotes

Inevitably, there are a number of cons to instant-issue insurance coverage, and these need to be considered against the advantages to ensure that a customer is seeking the finest sort of underwriting for their circumstance. While it is tough to generalise the response to the concern of whether something should be advised to a customer in monetary planning is virtually always, "It depends" there go to least a few crucial areas to consider to identify whether instant-issue term protection makes sense.

If we're considering situations where prospective outcomes are some coverage and no coverage, then a minimum of getting some insurance coverage in position is tremendously useful to the customer and those that would certainly be detrimentally affected by their premature death. While it may be less usual than the choice, there are times when clients are the ones driving the acquisition of insurance policy.

Instant Quote Life Insurance

In this instance, the behavioral obstacles to obtaining protection in area are most likely much less of a threat. If a customer is intrinsically motivated to obtain coverage in place, then they'll be a lot more inclined to press via obstacles, even if it suggests reactivating the underwriting process with one more business. As kept in mind formerly, there could still be advantages to instant-issue protection to consider, such as the decreased risk of finding out something new about a client throughout underwriting, but total behavioral benefits are significantly decreased.

Client, I'm recommending that you buy instant-issue coverage. This insurance coverage would cost you about $50 even more monthly than some generally underwritten protection, which traditionally underwritten insurance coverage would also have monetary benefits such as being exchangeable to permanent insurance if you choose. That stated, I do not assume the benefits are worth the additional problem in your instance.

By comparison, taking a more paternalistic method could lessen prospective behavioral barriers, aiding the client obtain the coverage they require much more effectively. Consider this different disclosure: Mr. and Mrs. Client, there are some options to possibly obtain some insurance coverage in location that could be more affordable and have a few benefits, however those methods need a medical examination and some added headaches that I do not think make the benefits worth the expenses in your scenario.

If a customer has $1 countless term insurance policy in location however is bumping as much as $2 million, after that perhaps, the lack of follow-through and various other dangers will most likely be reduced. Additionally, assuming the initial protection was traditionally underwritten, the client ought to comprehend the procedure and recognize what it requires.

There's likewise a lot more unpredictability about the process and the customer's determination to persevere. If a client is making their very first insurance coverage acquisition, then instant-issue term insurance policy could be a fantastic area to begin. An additional consideration here is that the client would not be locked into an instant-issue policy permanently.

It's worth considering the degree to which we are 'enhancing' below. For lots of clients that are first dealing with a consultant and strolling in with a messy situation (no estate docs, extinction insurance, no tax planning, and so on), going from no life insurance coverage to some life insurance coverage is much more valuable than going from some life insurance coverage to ideal life insurance policy.

Cheap Instant Life Insurance

Our leading choices for immediate life insurance coverage are Brighthouse Financial, Foresters Financial, and Legal & General America. Trick takeaways Instantaneous life insurance policy enables your application to be approved the very same day you use. A conventional life insurance policy application can take up to six weeks for authorization. You normally need to have very little wellness issues to make an application for instant life insurance policy, due to the fact that there's no medical examination.

Expense Using a mix of inner and outside rate data, we quality the expense of each insurance firm's premiums on a range from least pricey ($) to most costly ($$$$$). Get quotesWhy we picked itBrighthouse Financial supplies competitive prices, detailed coverage, and application choices in as little as 24 hours, making it an excellent choice for people that desire to obtain life insurance protection without having to take the medical test.

2025 Policygenius honor winnerPolicygenius score Our proprietary rating method takes numerous factors into account, including client satisfaction, expense, monetary strength, and policy offerings. See the "approach" section for more details. AM Finest score AM Best is a worldwide credit rating firm that ratings the monetary stamina of insurance companies on a range from A++ (Superior) to D (Poor). Cost Using a mix of inner and outside rate information, we grade the expense of each insurer's premiums on a range from least expensive ($) to most costly ($$$$$).30+ year termsAll 50 statesNo-medical-exam optionGet quotesWhy we picked itLegal & General America, which likewise operates as Banner Life and William Penn, has several of the longest term lengths as much as 40 years and the majority of affordable life insurance prices offered, also for individuals with a history of medical problems.

You'll complete a health and wellness interview over the phone first, however if you have a much more complex medical history, the business might ask for a medical examination. Immediate life insurance detailsMax insurance coverage limitation: Up to 40 times your revenue for people age 20 to 29; 30 times your income for people age 30 to 39; 20 times your income for people age 40 to 49; 15 times your earnings for people age 50 to 59Included bikers: Accelerated survivor benefit motorcyclist, term conversion, optional child life insurance policy motorcyclist, and an optional waiver of premium biker (an add-on that allows you to keep your plan if you end up being impaired and can no more pay your costs)Repayment: EFT financial institution draft only (checks permitted reoccuring payments)Protection limitation: As much as $2 million Policygenius score Our proprietary rating technique takes numerous variables into account, including customer fulfillment, expense, financial strength, and plan offerings.

{kind=link}

Latest Posts

Does Medicare Cover Funeral Costs

Instant Whole Life Insurance

Life Insurance Quotes Instant